JD Sports Update

We look at Previous tournament and CWC Performance for JD Sports and its Key Partners

Please see disclaimer at the bottom

Source: Marketwatch

Introduction

The recent Club World Cup gave us an insight into how JD Sport is positioned in terms of vendor relationships and catalogue for the next year. It is vital that the company sources the right inventory from Nike, Adidas, and Puma to cater to demand spikes and customer preferences. We decided to look at attendance and streaming trends we saw during the tournament while comparing the catalogues and pricing for all stakeholders in the apparel sector that were selling relevant items. This helps us assess JD’s competitive position going forward and seeing whether it can take advantage of its duopoly structure with Dick’s Sporting Goods.

Heat around the CWC

The CWC, held across the United States from June 14 to July 13, 2025, drew an average attendance of 39,557—a figure that pales in comparison to any World Cup since Chile 1962. The low point was a meagre 3,412 fans (just 13% of stadium capacity) for the Ulsan HD versus Mamelodi Sundowns clash in Orlando, Florida. Blame fell on a mix of factors: inconvenient midweek kick-off times, initial ticket prices that could make your wallet wince, scorching summer heat, and even whispers of Immigration and Customs Enforcement raids spooking some attendees. To counter this, FIFA adopted a dynamic pricing model, a staple in US sports, where ticket costs fluctuated like a volatile stock. For example, Chelsea’s semi-final against Fluminense saw standard admission tickets plummet from £350 to under £10 in a single week, boosting attendance to 70,556 for that match. This pricing pivot filled seats but highlighted the challenge of sustaining demand.

Streaming, however, tells a more compelling story. In the UK, Chelsea’s 2-0 victory over Los Angeles FC drew a peak audience of 1.6 million in the UK, while Real Madrid’s match against Al-Hilal captivated 1.1 million viewers. In Saudi Arabia, 1.5 million fans tuned in at 4am local time to watch Al-Hilal upset Manchester City 4-3—an empty freeway on a Friday night speaks volumes about the passion. Why does streaming success matter? In the sports industry, it’s all about storytelling. A gripping narrative—think underdog triumphs or star-studded showdowns—fuels fan engagement, which in turn drives merchandise sales. JD, as a leading retailer for brands like Nike, Adidas, and Puma, thrives when fans are emotionally invested enough to buy the latest kits or sneakers.

Enter sponsorships, the unsung heroes of this story. Adidas, the CWC’s official sponsor, also backs heavyweights like Bayern Munich and Real Madrid, ensuring its logo is plastered across the tournament’s most iconic moments. This dual role amplifies brand visibility, which is gold for retailers like JD, who stock Adidas’ latest gear. A well-told story needs a hero, and Adidas’ sponsorship ensures its products are front and centre, whether it’s a Bayern striker’s boots or a Real Madrid jersey flying off JD’s shelves. With 2.49 million total attendees across 63 matches and strong streaming numbers, the CWC has created a global stage for these brands, potentially translating into higher foot traffic and online sales for JD.

In short, the CWC’s mixed attendance underscores pricing and logistical challenges, but its streaming success and Adidas’ strategic sponsorships weave a narrative that could propel JD’s profits. If fans keep streaming and buying into the story, JD’s stock might just score the winning goal.

Background on Partner Performance and Strategy

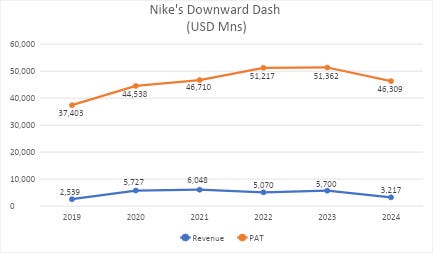

Nike

Nike has made it a point since the start to perfect this factor, endorsing rising stars like Mbappé and cup finalists PSG whereas Puma looks elsewhere to former champions Manchester City. One of the biggest sponsorship deals was back in 2017 when Nike signed current champions Chelsea for a whopping £900 million till 2032. Despite being a market leader, the company is in a bit of a pickle with sales dropping 10% to $46 Billion USD in FY24. Brand wise converse reported a 19% reduction followed by the same number for Nike driven by a 12% slump in footwear sales and 6% through apparel. This decrease is not particular to just one geographical area, but worldwide. China came out on top with revenue down 13% followed by Europe with 10%, NA 9% whilst the rest of the world (Asia Latin America) reduced 7%. The brand began restructuring after such numbers were posted starting with Converse, Aaron Cain to take the reins being with the company for 21 years taking over Jared Carver. With Elliott Hill taking charge of the Nike brand, he introduced a new strategy called Win Now which focuses on 5 sports disciplines; basketball, football (soccer), running, training and sportswear. This will be targeted across US, China and the UK with New York, Los Angeles, Shanghai, Beijing and London as the centre of attention.

Despite its dominance in the sports industry, Nike faces a tough climb to reclaim its edge. Regaining retail presence requires new partnerships, while restoring its reputation for ground breaking products and inspiring campaigns demands significant effort, especially after losing key talent. Adapting outdated strategies tied to overhyped trends like digitalization is achievable, but the real challenge lies in reviving the core values that defined its success. Nike’s true strength has always been its culture—a relentless, sport-driven drive to compete and inspire. Refocusing on this ethos is the key to its turnaround.

On the other hand, Adidas is gearing up to crown Lamine Yamal as its new brand face, orchestrating a symbolic handoff from Lionel Messi, showcasing storytelling as we spoke about earlier. With Yamal’s long-term FC Barcelona contract and his new No. 10 shirt, Adidas is set to launch a bold marketing campaign post-2026 World Cup, spotlighting both stars to cement Yamal as the next global ambassador for Adidas Football.

Adidas Financial Snapshot FY24

Adidas delivered a solid performance in FY24, balancing strong brand momentum with a challenging economic backdrop. The global sports footwear and apparel giant saw wholesale remain its dominant sales channel, contributing 60% of net sales (up from 59% in 2023), while direct-to-consumer (DTC) channels, including retail and e-commerce, accounted for 40% (down slightly from 41%). The company expanded its physical footprint to 1,933 stores worldwide, with 838 concept stores and 1,095 factory outlets, up from 1,863 total stores in 2023. On the product front, Adidas leaned into its football heritage, relaunching the iconic F50 boot for its 20th anniversary and introducing third jerseys made from 100% recycled polyester for top clubs like Bayern Munich, Manchester United, Juventus, Arsenal, and Real Madrid. The Bad Bunny and Lionel Messi collaboration reimagined the Gazelle and F50 silhouettes, blending street style with performance. Strategic sponsorships, including the FIFA Club World Cup, UEFA Champions League, and new partners like the Mercedes-AMG PETRONAS F1 team, amplified brand visibility, with stars like Jude Bellingham and Messi fronting campaigns like “You Got This” during UEFA EURO and Copa América.

Segmental Analysis Adidas FY24 (Euro Mn)

Other Businesses includes the business activities of the Y-3 label and other subordinated businesses which are not monitored separately by the chief operating decision-maker

Operationally, Adidas’ supply chain remained Asia-centric, with Vietnam leading at 27% of sourcing volume, followed by Indonesia (19%) and China (16%), totalling 92% of production. However, potential tariffs amid rising geopolitical tensions could disrupt this Asia-heavy supply chain. Looking to 2025, Adidas faces a mixed outlook: advanced economies are projected to grow sluggishly at 1.7%, while developing markets offer brighter prospects at 4.1%. Elevated inflation, high interest rates, and geopolitical risks may curb consumer spending, making adaptability key. Yet, with its robust sponsorship portfolio and innovative product launches, Adidas is well-positioned to navigate these challenges and keep scoring with consumers.

Puma

PUMA kicked off 2025 with a mixed performance, balancing modest growth against a tough global backdrop. Currency-adjusted sales edged up 0.1% to €2,076.0 million, though reported sales dipped 1.3%. EMEA shone with a 5.1% rise to €891.7 million, fuelled by double-digit growth in emerging markets, while the Americas slipped 2.7% to €753.7 million, dragged down by North America despite Latin America’s strong gains. Asia/Pacific faltered, with sales down 4.7% to €430.5 million, reflecting weakness in Greater China.

The wholesale channel, PUMA’s bread and butter, fell 3.6% to €1,529.5 million, hit by softness in the U.S. and China. Meanwhile, the direct-to-consumer (DTC) business sprinted ahead, growing 12.0% to €546.5 million, with e-commerce soaring 17.3% and retail stores up 8.9%. DTC’s share climbed to 26.3% from 23.5% last year, signalling a shift toward direct engagement. Footwear led product growth, up 2.4% to €1,186.0 million, driven by running and basketball lines, while apparel and accessories lagged, down 1.5% to €594.3 million and 5.7% to €295.7 million, respectively.

Profitability took a hit, with the gross margin slipping 60 basis points to 47.0%, pressured by currency headwinds and prior-year inventory gains, though be

tter sourcing and product mix cushioned the blow. Operating expenses rose 7.1% to €904.9 million, driven by DTC investments and higher depreciation, pushing the OPEX ratio to 43.6% from 40.2%. Adjusted EBIT, excluding €18.0 million in one-time restructuring costs, plunged 52.4% to €75.7 million, and reported EBIT fell 63.7% to €57.7 million, yielding a 2.8% margin. Net income collapsed to €0.5 million from €87.3 million, with earnings per share at €0.00, down from €0.58.

Working capital grew 12.8% to €2,081.6 million, with inventories up 16.3% to €2,076.1 million due to goods in transit. PUMA also completed a €100 million share buyback, repurchasing 2,816,714 shares at €35.50 each, signalling confidence in long-term value. On the brand front, PUMA’s Premier League partnership and eco-friendly product push (90% recycled materials in 2024) kept its edge sharp.

Looking to 2025, PUMA expects low- to mid-single-digit sales growth and an adjusted EBIT of €520 million to €600 million, down from €622.0 million in 2024, as it navigates one-time costs of up to €75 million from its “next level” efficiency program, which should yield €100 million in EBIT gains. With €300 million earmarked for retail and digital investments, and potential U.S. tariffs looming, PUMA’s agility will be key to outpacing a volatile market.

JD Sports Performance After Previous CWC

JD Sports Fashion Plc delivered a solid FY24, with revenue climbing 2.7% to £10.4 billion, outstripping the sportswear market’s 2-3% growth. Organic sales surged 9%, fuelled by 3.8% like-for-like growth and 468 new store openings under the “JD First” strategy. The outdoor segment (5% of revenue, including Go Outdoors, Blacks, and Millets) dipped 2.1%, with a 2.6% like-for-like decline, pressured by mild UK autumn/winter weather. North America rose, with 2023 sales hitting $3.9 billion and $361 million in profit, driven by Shoe Palace and DTLR acquisitions. These US acquisitions, Shoe Palace and DTLR, each generated £0.5 billion in revenue, transformed into profit engines, with Shoe Palace yielding £50 million and DTLR £20 million in annual profit. These deals boosted US sales by $1 billion and profits tenfold over historical levels, showcasing JD’s operational prowess. Europe grew below double digits, hampered by supply chain costs from dual UK-Netherlands warehousing. JD’s market share held strong at 30% in the UK, 10% in Europe, 5% in North America, and 10% across the UK, Ireland, and Australia combined.

Capital expenditure reached £570 million (5.5% of revenue), with 60% allocated to store openings, reinforcing “JD First” and “Complementary Concepts.” The Heerlen distribution centre, operational manually in 2024 and automating in 2025, will enable next-day D2C deliveries by 2026, slashing dual-running costs. A planned APAC warehouse within 12 months will bolster growth. The JD STATUS loyalty program, with 5.1 million US customers (£1 billion sales, 38% attachment rate) and 1.2 million UK downloads (£0.2 billion sales), resonated with young adults (16–24), 60% of whom plan to increase athletic leisure spending. JD’s omnichannel strength and 5x market-average growth over five years position it to keep scoring for investors.

JD Sports

Coming back to JD Sports Fashion Plc powered through FY25 with a 10.2% revenue surge to £11.46 billion, fuelled by 5.8% organic sales growth and £852 million from the acquisitions of Hibbett and Courir. Footwear, the star player, drove 15.2% growth to £6.82 billion, boosting its revenue share to 60%—a 3%-point increase—largely due to Hibbett’s sneaker-heavy mix. Apparel, however, grew a modest 4.2% to £3.55 billion, with its share dipping 1% to 31%, hit by wet weather in the UK and Europe that triggered summer discounts. Accessories rose 4.8% to £702 million, holding a 6% share, while other categories like gym memberships added 3%. Geographically, North America led with 40% of revenue, followed by Europe (30%), the UK (25%), and Asia Pacific (5%). Store sales dominated at 79%, with online sales at 26% in the UK and 15% in Europe, returning to pre-pandemic levels as shoppers flocked back to physical stores.

Operationally, JD expanded to 4,850 stores globally, adding 1,533 stores, primarily via Hibbett and Courir, while opening 311 new stores and closing 263 non-core locations. The company optimized its supply chain, closing the UK’s Derby distribution centre and leveraging “ship from store” capabilities in Europe. The Heerlen distribution centre in the Netherlands, set for full operation by 2026, will enhance European efficiency, while Morgan Hill in the US will become a multi-brand hub by FY26, promising cost savings. However, potential US tariffs, could challenge this Asia-reliant supply chain. Operating costs rose 11.6% to £4,423 million, driven by new stores, Heerlen’s dual-running costs, and investments in cybersecurity and the JD STATUS loyalty program. Excluding acquisitions, costs grew 7.8%, outpacing organic revenue growth.

The JD STATUS loyalty program, now boasting 8 million active accounts globally, including 2.6 million in the UK, drove a 30% sales mix in stores, with members spending 24% more and shopping 10% more frequently. Launched in France during the 2024 Paris Olympics, Ireland in November 2024, and Poland and Romania in 2024-2025, it lifted in-store order values by 30% across these markets. Digital investments continue, with a website re-platforming set for the US by late 2025, followed by the UK and Europe. Despite a 4% drop in profit before tax and adjusting items due to acquisition financing and growth investments, JD’s market share in global sportswear climbed 0.8% to 6.5%.

Total revenue climbed 10.2% to £11.46 billion, but the UK lagged, dipping 4.1% to £3,205 million, largely due to shedding non-core businesses over the past two years. Europe, meanwhile, powered up 13% to £3,510 million, boosted by two months of Courir’s contribution. North America stole the show, surging 24% to £4,242 million, fuelled by six months of Hibbett’s sneaker-heavy sales. Asia Pacific was tempered by a hit from exiting non-core operations, though newer markets showed promise. This reshuffled JD’s revenue mix, with North America leading at 37%, followed by Europe at 31%, the UK at 28%, and Asia Pacific at 4%, reflecting a more balanced global footprint.

Strategy and Pricing

With a surge in football merchandise demand, likely boosted sales of Nike’s Chelsea jerseys, which JD sold at competitive prices (e.g., £100.00 vs. Nike’s $95.00 USD), reinforcing its edge in capturing fan-driven demand.

The 2025 FIFA Club World Cup, wrapping up on July 13, 2025, in the US, sparked a frenzy for football merchandise, offering a prime lens to compare pricing strategies of JD Sports and manufacturers Nike, Adidas, and Puma. JD Sports, a retail powerhouse, flexed its pricing muscle to capture fans’ wallets during the tournament. Typically, JD maintains steady prices for items like Chelsea’s 2025/26 home jersey before the event, listed at £100.00 in the UK on their website. During the Club World Cup, JD likely rolled out promotions—think 20% off or free shipping—to boost sales, potentially dropping the jersey to £80.00 ($100.00 USD), aligning with their strategy of competitive and promotional pricing to outshine rivals, as noted in their FY25 results. Post-tournament, clearance sales with up to 50% discounts likely cleared excess stock, a tactic JD employs to keep inventory lean.

In contrast, Nike, the manufacturer behind Chelsea’s kit held firm on premium pricing, listing the jersey at $95.00 USD on their US site. With no major discounts during the tournament, Nike banked on brand prestige and Chelsea’s victory to drive direct sales, as their annual report emphasizes exclusivity over price cuts. Adidas, the Club World Cup’s official sponsor, priced comparable club jerseys, like Manchester United’s, at $100.00 USD, maintaining high prices to leverage their sponsorship and brand value, per their 2024 annual report. Puma, known for competitive pricing, offered jerseys like Borussia Dortmund’s at $80.00 USD, undercutting Nike and Adidas to appeal to budget-conscious fans. JD’s ability to offer the Chelsea jersey at a potentially lower price point during promotions gave it an edge over Nike’s steadfast $95.00, while Adidas and Puma’s higher or competitive MSRPs reflect their focus on brand positioning. With potential US tariffs looming, JD’s retail flexibility could prove crucial in navigating cost pressures, making it a compelling play in the sportswear market.

Conclusion

JD Sports Fashion Plc’s Forward P/E ratio stands at an attractive 7.3x, signalling potential undervaluation compared to peers like Dick’s Sporting Goods, which trades at nearly double that multiple. Historically, JD’s valuation spikes during major football tournaments, such as the 2023 Club World Cup in Jeddah, driven by surging demand for merchandise.

JD Sports Fashion Plc remains a standout investment, driven by its aggressive global expansion and robust financials. The company’s dedicated property team has fuelled strategic store openings, adding 1,533 locations in FY25, whilst recently launching into new Canadian markets, to capture prime retail spaces in over 30 countries. This aligns with JD’s “JD First” pillar, which, alongside acquisitions like Hibbett, propelling organic sales growth and a 10% sales surge in FY25. However, JD’s heavy reliance on Nike, with top-sellers like the Air Force 1 and Chelsea jerseys driving sales during the 2023 Club World Cup, poses risks as market trends shift toward running, led by On Holding’s rising popularity. To stay ahead, JD must diversify its brand mix to capitalize on this demand. With the 2026 FIFA World Cup looming, JD’s forward P/E of 7.3x—half that of peers like Dick’s Sporting Goods—signals undervaluation, especially given historical valuation spikes during tournaments. Sound financials, strategic pillars, and upcoming football tailwinds make JD a compelling buy for investors.

Disclaimer

ATTENTION - PLEASE READ THROUGH THE FOLLOWING POINTS

The content provided in this newsletter is for informational purposes only and should not be construed as financial, investment, or other professional advice. The opinions and analyses expressed here are those of the author(s) and do not necessarily reflect the views of any affiliated organizations. While we strive for accuracy, we cannot guarantee the completeness or timeliness of the information presented.

Investment Risks

Investing in stocks and other financial instruments involves risk, including the potential loss of principal. It is important to conduct your own research and consider your financial situation and risk tolerance before making any investment decisions. Past performance is not indicative of future results.

No Recommendations

This newsletter does not constitute a recommendation to buy, sell, or hold any security or financial instrument. The author(s) may hold positions in the securities discussed. All information is provided "as is" without any warranty of any kind, express or implied.

Consult Professionals

Before making any financial decisions, you should consult with a licensed financial advisor, tax professional, or other relevant experts. The content of this newsletter should not be used as a substitute for professional advice tailored to your specific situation.

Limitation of Liability

The author(s) and publisher of this newsletter shall not be liable for any errors or omissions, or for any actions taken based on the information provided herein. You agree to hold the author(s) and publisher harmless from any claims or damages arising from your use of this newsletter.

| A guest post by

|