Hollywood Bowl Report

A More Balanced Alternative to Bowlero Corp?

Please See Disclaimer at the bottom

Source: Hollywood Bowl Website

Introduction

After looking at a few large caps, we shifted our focus to the small caps, in search of brilliant yet simple businesses with significant white room available. Value Investors nowadays often go searching for complicated businesses while overlooking those with a strong financial track record which offer the kind of predictability we all crave. One popular name among UK investors that fits this profile is Hollywood Bowl which seems to be unknown the counterparts in North America who are only aware of Bowlero when it comes to bowling stocks. The Company is the UK’s largest ten pin bowling operator and offers standard 10 pin bowling, food & beverages, amusements, and mini golf courses through its centres in UK and Canada. It is listed as BOWL on the London Stock Exchange where it went public in 2016.

Bowling is an old pastime of the human civilisation. We can authentically trace its history back over 7000 years to Ancient Egypt where the grave of a child showed implements for playing a game similar to modern tenpins. According to some authorities, its place of origin in Europe is Northern Italy where the Helvetti people of the Alpine region were believed to have played a game similar to the present-day Italian game called Boccie. The modern-day form of Bowling was originally played by the Dutch as well as the Germans and the Swiss who used a single board about 12-18 inches wide and about 20-30 yards in length all on a board platform from 36-48 inches square. After further developments, the first indoor bowling lane opened in London around 1455 AD.

The origins of Tenpin are thought to have come into being between 1820 and 1830. Legislators who banned 9 pin bowling as it was synonymous with gamblers in 1841 allowed Tenpin to grow. Bowling lanes existed on almost every block in Broadway, New York and it was around the 1860s, finger holes were cut in the 9” balls and tournaments and clubs gave rise to competitive bowling. The sports long history shows that leading operators are likely to grow and remain competitive as it has been a popular leisure activity throughout history. It is this sort of timelessness which attracts us to the sector.

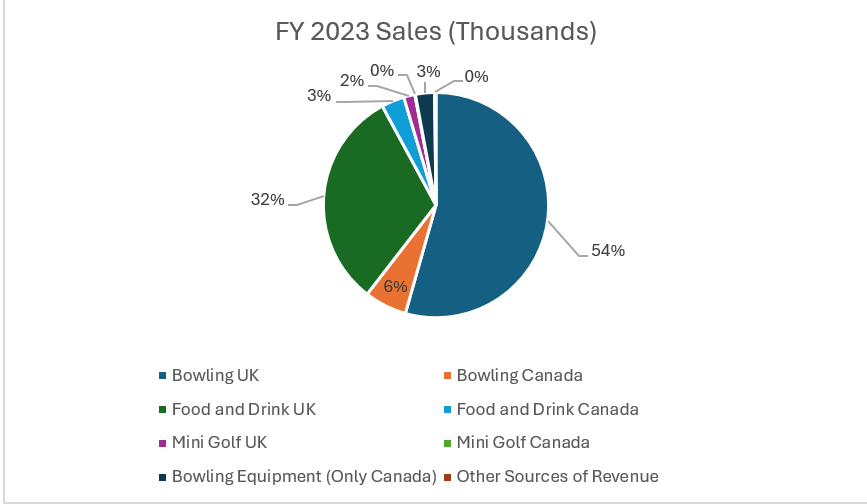

The company has 6 sources of revenues which are split geographically between UK and Canada. Its main and largest source of revenue is bowling from its Hollywood Bowl (UK) and Splitsville (Canada) centres. Food and Beverage (F&B) revenues come sales generated from restaurants and bars located in the bowling centres. Amusements sales come from the centre’s arcade and game machines. Hollywood Bowl also started to run Mini-golf operations under the Puttstars brand in the UK back in 2020 and runs a small service in Canada. The only revenue source exclusive to Canada is Striker Solutions which is a B2B supplier for bowling equipment.

Background of Hollywood Bowl

The Hollywood Bowl Group was formed in 2010 following the merger of certain bowling centres in the AMF portfolio with the Hollywood Bowl portfolio that was part of Mitchell and Butlers Group. CBPE Capital provided the equity funding to facilitate The Original Bowling Company’s purchase of Hollywood Bowl and units of AMF Bowling. A reorganisation was carried out with a roll up strategy being devised where existing centres would be refurbished under Hollywood Bowl and new centres would be purchased to undergo redevelopment. At this point, the combined entity had 41 centres. Additional capital was provided to add 3 new locations by CBPE Capital. The rebrand and refurbishment was based on customer feedback which resulted in the management team preferring smaller, more ‘boutique’ formats for their centres which can be seen today as it provided the best customer experience. With this strategy in mind, the new group under new private ownership began operating.

Fast forward to 2014, the group went through a friendly management buyout that was backed by Private Equity firm Electra Partners. At the time of the exit, the then Original Bowling Company was the largest 10 pin bowling operator in the UK with 44 sites. EBITDA had increased by over 60% with the technology investment and improved customer perception delivering improvements in both top and bottom line. In terms of the ROI, CBPE Capital achieved a 2.4x return on invested capital with an IRR of 24%.

An investment of £51 million was made by Electra with a combination of equity and debt being utilised. CEO Steve Burns also invested with his colleagues in the deal with the management team being a key part of the new ownership structure. Electra’s holding period saw a continuation of CBPE’s strategy of acquiring and opening new centres with refurbishment then taking place. In December 2015, the group purchased Bowlplex with 11 centres being added to the estate portfolio. The first 4 years of the group’s operation showed how PE can potentially profit from a purchase of Hollywood Bowl and, how it benefits operationally from being owned by 2 PE firms till date.

Hollywood Bowl went public on the 21st of September 2016 with a market capitalisation of GB 240 million. On the day of the admission, Electra was expected to receive cash proceeds of GBP 153 million from the sale of its equity investment as well as a repayment of GBP 22 million of debt instruments. The total equity return for Electra was 3.1x in cash plus a further 0.8x in shares, totalling a Money on Multiple of 3.9x and an IRR of over 90%. Its ownership stake decreased from 85% to 18% after the IPO with a lockup period being instated of 6 months. Electra then exited completely in April of the following year.

The management team did not sell their shares as the IPO was structured to allow Electra Partners to exit from its investment. The IPO raised £181 million with the majority of the amount going to investors. No new shares were issued by Hollywood Bowl which meant no new capital was raised making it a secondary offering where existing shareholders sold their shares to new investors. Management keeping their shares showed their long-term faith in the company which is evident till date as the same management runs the business.

Keep reading with a 7-day free trial

Subscribe to Saadiyat Capital to keep reading this post and get 7 days of free access to the full post archives.