From Rickshaws to Crossovers

How Sazgar Engineering Works Limited Became One of Pakistan’s Greatest Wealth Creators, and Whether That Run Can Continue

I. Introduction: A Stock That Should Not Have Existed

For most of its three-decade life on the Karachi Stock Exchange, Sazgar Engineering Works Limited was a quiet, almost ignorable company. It made rickshaws, those CNG-powered three-wheeled contraptions that ferry the bottom two-thirds of Pakistan’s urban population to work. It made wheel rims for tractors. It imported electric appliances under the Whirlpool name. Its financials were modest, its margins thinner than the sheet metal it stamped, and its capital base small enough that the entire company traded at roughly Rs. 83 million in market value as recently as November 2004.

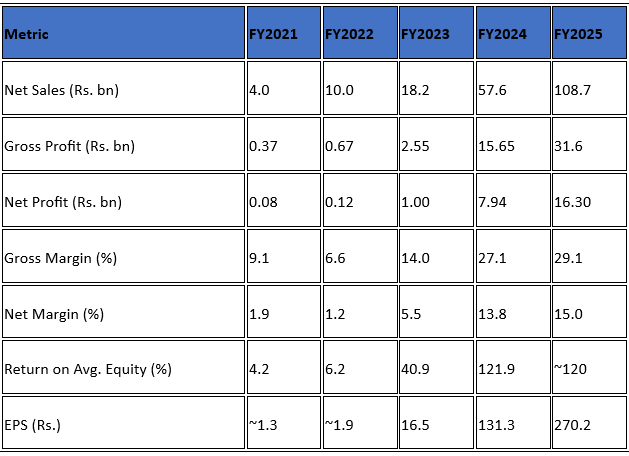

In May 2026, the same company is worth approximately Rs. 132 billion. Its trailing twelve-month revenue is over Rs. 142 billion, its net profit Rs. 18 billion, its return on average equity over 120 percent, and its earnings per share more than Rs. 300. Its all-time-high stock price of Rs. 2,487, reached in February 2026, sits roughly 450 times above the Rs. 5.47 low it traded at in April 2013. On a market-capitalisation basis, the company has compounded at over 41 percent annually for twenty-one years, a return profile that places it not merely among the best-performing Pakistani equities of its era but among the most extraordinary compounders any frontier market has produced in modern memory.

The puzzle is not just the return; it is the path. Sazgar did not get here by extending what it already did well. It got here by attempting something it had no business attempting, namely assembling Chinese SUVs in a market dominated for forty years by Toyota, Honda and Suzuki, and by being unusually well-positioned in its timing, its partner, and the cyclical position of the Pakistani consumer at the exact moment its product arrived. The question that should animate any serious investor reading the company’s filings today is whether what looks like genius was, in fact, a confluence of structural advantages that can be repeated, defended and compounded; or whether Sazgar has, like so many emerging-market darlings before it, captured a window that is already beginning to close.

This essay reconstructs how Sazgar arrived at its present state, what its financial statements actually reveal about the durability of its franchise, and what variables an institutional investor should watch over the coming five years to determine whether the compounding can persist. The broader subject, however, is not really Sazgar. It is what Sazgar reveals about the post-2020 evolution of Pakistan’s industrial economy: a country whose middle class is finally large enough to support genuine consumer aspiration, whose policy apparatus has, almost by accident, created the architecture for Chinese manufacturers to displace Japanese incumbents that grew complacent over four decades of tariff protection.