Fintech in Asia

We interview an Executive at a Fintech Company in a major market in Asia

Please see disclaimer below - this report is not investment advice

Source: IFLR

Executive Summary

In this interview, a senior executive from a major financial institution in Asia—backing a fintech company in an emerging market—walks us through the realities, constraints, and creativity that shape financial innovation on the ground. From infrastructure limitations to AI-led personalization, this conversation offers a front-row view into how fintech is being redefined in regions with very different starting points than Silicon Valley or London. What follows is a lightly edited transcript for clarity and flow.

Q: From the perspective of growth, how are strategies for scaling up different in emerging and developed economies in the context of fintech?

In emerging markets, our general focus as fintechs is on increasing adoption among our customers. These customers typically fall within certain socioeconomic segments— generally “SEC A” “SEC B” “SEC C”—and our approach differs from how developed markets engage theirs. Developed markets have established infrastructure, advanced credit scoring systems, and sophisticated credit products like credit cards and "buy now, pay later" options. They even offer interest-free payment schemes that we currently don’t have access to.

There are both minor and major differences in how we segment our customers. Our primary method of customer acquisition is through agents, which allows us to reach remote areas where internet availability is limited—4G or other connectivity is often unreliable in such locations. To overcome this, we partner with major telecom networks that help us penetrate these underserved regions.

Developed countries don’t typically face this challenge. They can simply advertise and acquire customers online. That’s one of the key distinctions—our hybrid model. The responsibility of customer acquisition doesn’t fall solely on the fintech. It involves telcos, banks, and even regulators, all of whom play a role in scaling fintechs in emerging markets. This is a common trend across nearly all countries in this segment. Growth is community-driven, not the result of a single entity acting alone.

Takeaway: The use of telecom networks as distribution and onboarding partners is a major differentiator in emerging markets. Investors should view these partnerships not as workaround strategies but as fundamental infrastructure for success in underserved regions.

Q: How do products differ between both markets?

A: Let’s take "buy now, pay later" (BNPL) as an example, comparing emerging markets and developed ones. In emerging markets, we don’t have access to customer information at the level that developed markets do. In developed regions, fintechs and banks operate within a highly integrated environment—everything is linked through open banking. They know your monthly expenditures, bills, income patterns—essentially, your full financial profile.

Emerging markets haven’t implemented open banking yet, so we lack access to the dynamic, real-time information that developed markets rely on. For instance, in a developed market, a BNPL provider can easily assess whether a customer can manage a 0% installment plan. For us, it’s a risk—we often don’t know. It becomes a chicken-and-egg situation: the fintech doesn’t want to make a wrong call, and neither does the customer.

Beyond BNPL, developed markets offer bespoke investment platforms and deeply integrated credit products across banks and fintechs. In contrast, emerging markets are still focused on meeting basic financial needs—insurance, bill payments, small loans. Many people still visit physical bank branches to pay their bills in person.

So, our core mission is digitalizing these fundamental services. Remittances are also a significant part of our economies, and capturing and optimizing those flows is a key driver for many fintechs operating in this space.

Takeaway: Emerging market fintechs must often build trust before introducing advanced products. This step-by-step evolution reflects both user readiness and regulatory maturity.

Q: What is the level of sophistication of the credit and financial models at fintechs in emerging markets?

A: This is perhaps the most critical aspect of what we do—providing access to credit for those who have never had it. In emerging economies, banks typically serve the SECA or SECA+ income segments—customers with stable financials who can absorb structured lending. Fintechs, on the other hand, are working to unlock credit for middle-income and lower-middle-income customers. That’s our North Star metric: onboarding as many of these individuals as possible for lending.

We use dynamic credit scoring algorithms, often built from real-time in-app behavior, so customers don’t have to go through traditional credit checks. We’re also collaborating with other fintechs and banks in the ecosystem, sharing data and collectively moving toward an open banking environment.

Internally, we’ve built teams focused on leveraging AI and machine learning to better understand customer choices, spending habits, and risk behavior. While our current product set is still limited, our models are evolving rapidly. We expect to have a much more sophisticated lending infrastructure in the coming years. We’re not there yet—but we’re accelerating quickly.

Takeaway: AI and ecosystem collaboration are acting as accelerators for financial inclusion. A shift toward data-sharing alliances may position certain fintechs as early market leaders.

Q: How do you balance between growth, profitability and regulatory compliance?

A: Particularly in emerging economies, the regulatory culture is surprisingly progressive. Regulators want more people to be financially included because it benefits the broader economy. For us, profitability is achieved at the unit economics level—by being prudent. We're not aiming for large profit margins; instead, we ensure that each user makes financial sense. If every user is viable, the business as a whole sustains itself.

This means we don’t chase vanity metrics. We operate lean and focus on delivering real value through our app. Customer retention is critical—we need users to enjoy the experience, engage with it regularly, and avoid churning.

Our relationship with regulators is also essential. In emerging markets, approvals aren’t automatic; you have to understand how the system works and navigate it carefully. We also diversify our revenue streams—we're entering investment segments, using debt cautiously, and maintaining a lean internal team.

In short, we balance growth and sustainability through structure and discipline—not through unchecked expansion.

Takeaway: Unit economics clarity is especially important where capital is expensive and venture money is cautious. This approach reflects a shift toward more disciplined scaling.

Q: How has backing from a major financial player in Asia influenced your long-term strategy and the way investors perceive you?

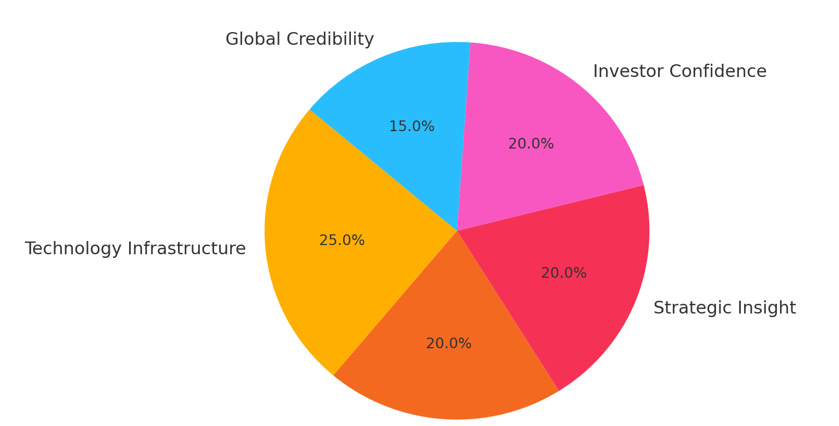

A: Everyone knows this major financial player from Asia—it's one of the most recognized brands globally. Their investment brings significant credibility, not just with external investors but also within our own teams. The technology they bring into the company is world-class. In fact, most people don’t even realize how advanced some of their systems are.

But the greatest value lies in their operational guidance. They’ve already done much of what we aspire to do—they’ve tested at scale, succeeded in similar markets, and, crucially, they’re not just investors; they’re experienced operators. So when we encounter a challenge, chances are they’ve already faced and solved it. That sharpens our planning process.

This support strengthens our board and boosts investor confidence. Everyone knows we’re not navigating this alone. Their reputation also extends across the broader region, giving us a strong foundation when we present internationally.

Takeaway: Strategic investors can de-risk fintech ventures in uncertain markets by offering proven frameworks, elevating both execution speed and valuation.

Figure 2: Strategic Contributions of the major financial player in Asia

Q: Where do you see the most exciting product innovation in fintech today?

A: Embedded finance and lending are absolutely essential. Embedded finance means everything happens within a single flow—no redirections, no switching between apps. You’re purchasing a product, and the credit option appears right there on the same page. This kind of frictionless experience is especially crucial in emerging markets; without it, many users simply drop off.

With AI layered on top, the experience becomes even smarter—it’s no longer just a payment option, it becomes a personalized recommendation. Lending is also evolving. We’re working to make credit more accessible in ways that haven’t existed before.

Takeaway: Embedded finance reduces friction in the customer journey, and its adoption signals a critical infrastructure layer that may underpin emerging market fintech over the next decade.

Figure 3: Embedded Finance Ecosystem in Emerging Markets

Q: How do you think AI and real-time data will reshape financial infrastructure in emerging markets?

A: AI is already transforming how we operate, and we’re only scratching the surface. One of the most immediate impacts has been on credit scoring. Traditional models rely on formal banking history—something millions of people in emerging markets just don’t have. But now, we can assess creditworthiness using alternative data: behavioral patterns, smartphone metadata, social graph signals, even how someone interacts with mobile apps. That opens up access to credit for people who’ve been invisible to the formal financial system.

Fraud detection is another game-changer. AI allows us to detect anomalies in real time—patterns that would be impossible to catch manually. In one case, we uncovered a coordinated fraud ring that had been flying under the radar for months. That’s the kind of edge AI gives you when deployed well.

Operationally, AI helps us stay lean. In markets where margins are tight and infrastructure is often fragmented, automating manual processes isn’t just a convenience—it’s critical to survival. AI can manage underwriting, customer onboarding, KYC, even support chat—all with minimal human intervention.

That said, AI isn’t a magic button. The models still need to be trained on local data, which isn’t always easy to gather or standardize. Bias and data quality are real concerns. But the foundations are in place. Over the next decade, as infrastructure improves and data becomes more available, we’re going to see AI fundamentally reshape how financial services are built and delivered in emerging markets. It’s not just about catching up with developed markets—it’s about leapfrogging them.

Takeaway: Fintechs leveraging AI will enjoy faster product feedback loops and better risk-adjusted returns. First movers may define regulatory standards in this space.

Q: What does product localization mean for you when entering new emerging markets?

A: Localization is much more than just translating an app into the local language. It’s about deeply understanding the context and fabric of the market you're entering. That means asking hard, practical questions: What are the cultural attitudes toward money? Do people feel comfortable taking on debt, or is borrowing seen as taboo? Are they more likely to trust formal banks, or do they rely on informal savings groups, family networks, or even cash under the mattress?

You can’t assume that a feature that works brilliantly in one market will resonate in another. Sometimes we’ve had products that we were incredibly excited about internally—beautifully designed, technically solid—but we’ve had to hold back because the customer wasn’t ready. Timing, trust, and behavior matter. So we start small: we test, we pilot, we gather feedback, and only then do we scale. It’s an iterative, humility-driven process.

Localization also touches every layer of the product stack. Pricing models need to reflect local income levels and financial habits. Onboarding flows need to feel intuitive to someone who may be less digitally native. Even the tone and structure of customer support scripts need to reflect local language norms, values, and sensitivities. We think of it as “priority-first” design—starting from the customer’s reality—not as a “lift-and-shift” strategy from another market.

Ultimately, true localization is about respecting the customer. It’s not about exporting a fintech product—it’s about embedding it in people’s lives in a way that makes sense to them.

Takeaway: Localization extends beyond UX—it influences product-market fit, retention, and compliance. Getting it right is a form of strategic defensibility.

Q: What is fintech's biggest structural advantage over traditional financial institutions today?

A: It’s definitely agility—both in mindset and in operations. Unlike traditional financial institutions, we’re not burdened by decades of legacy infrastructure. There are no outdated core banking systems, no siloed departments with conflicting priorities, and far less bureaucracy slowing down decision-making. We’re built for speed, experimentation, and iteration.

That agility extends beyond technology. Structurally, we’re not confined to a single revenue model like deposit-taking and lending. We can build diversified income streams—from transaction fees to subscription models to partnerships with third-party platforms. That flexibility gives us room to innovate in ways that banks often can’t.

Data is another key advantage. We don’t just collect it—we act on it. Our products are designed to respond to user behavior in real time. For example, we can dynamically personalize an interface based on how a user engages with the app. Someone new to digital finance might see a simpler, more guided experience, while a power user might get advanced features front and center. Traditional banks just aren’t wired to deliver that level of customization—they’re still serving everyone the same dashboard, the same forms.

And we do all of this with a much leaner cost structure. Fewer branches, fewer legacy staff, more automation. That cost advantage translates into more competitive pricing for customers and more headroom for us to reinvest in product.

In emerging markets, this agility is even more critical. These markets evolve quickly—consumer behaviors shift, regulations change, infrastructure gaps close rapidly. The ability to adapt in near real time isn’t just nice to have—it’s what allows us to stay relevant and win.

Takeaway: Fintech's leaner model allows for faster adaptation to consumer behavior shifts—especially critical in volatile, inflation-prone markets.

Q: Will the future of fintechs be standalone firms or more hybrid partnerships?

A: I think the future is going to be overwhelmingly hybrid. While there will always be room for standalone fintechs—especially those focused on deep tech or infrastructure layers like credit scoring, KYC, or fraud analytics—the real scale and sustainability will come from partnerships.

Banks, for example, have the capital, the licenses, and the regulatory experience. But they often lack the speed, agility, and user-centric design that fintechs excel at. Telcos bring something equally valuable: massive, pre-existing customer bases, distribution networks, and in some cases, mobile money platforms that already have consumer trust. When you combine these with a fintech’s technical stack and UX capabilities, you get a powerful equation for growth.

We’re already seeing this model play out in many markets. Whether it’s digital wallets plugging into telecom infrastructures or lending platforms partnering with banks for underwriting and compliance, the momentum is clearly toward collaboration. It’s faster to market, cheaper to scale, and more resilient across regulatory shifts.

Regulators are also nudging in this direction. They generally prefer shared-risk ecosystems where no single player dominates every part of the value chain. Partnerships can distribute liability and oversight more evenly, which makes regulators more comfortable and encourages innovation within guardrails.

So yes, hybrid is the future—and not just as a tactic, but as a strategy. Ecosystem thinking is how we move from niche fintech use cases to widespread, mass-market adoption. The winners will be those who can build bridges, not just products.

Takeaway: Collaborative ecosystems will become table stakes for scale. Investors should evaluate not just a fintech's tech, but its ability to forge and maintain key partnerships.

Q: What key metrics or signals do you think investors are undervaluing when it comes to fintech firms right now?

A: Investors have definitely become more cautious after the 2020–21 bubble period. There’s been a clear shift from chasing user growth at all costs to looking for sustainable unit economics, compliance readiness, and clear paths to profitability. That’s a good correction. But in that process, I think one thing many investors still undervalue—especially in emerging markets—is how proactively a fintech engages with the regulatory and broader financial ecosystem.

Growth is important, but in these markets, it’s not just about how fast you can scale—it’s about how responsibly and strategically you operate. For example, is the company actively engaging regulators? Are they helping to shape policy, pursuing licenses early, or collaborating with central banks and industry bodies on pilot programs or sandboxes? These are subtle signals, but they speak volumes about a fintech’s long-term viability.

In emerging markets, the infrastructure is often still forming. Fintechs aren’t just building businesses—they’re helping to lay the foundation for the broader financial ecosystem. The most impactful firms are those that don’t just take advantage of market gaps but actually help close them. They don’t operate in isolation—they bring others along, whether by building rails that other players can use, pushing for interoperable standards, or setting examples in governance.

That kind of ecosystem-minded leadership is hard to quantify with a single metric, but it matters deeply—especially over the long term. Investors who pay attention to how a fintech behaves in its market, not just how fast it grows, are the ones who will spot the durable winners. The real value isn’t just in capturing market share—it’s in shaping the market itself.

Takeaway: Early signs of ecosystem leadership—like regulator advocacy and partnership-driven innovation—may be stronger long-term success indicators than growth alone.

Q: Where do you see your sector—financial technology in emerging markets—five years from now?

A: Ideally, we’ll see embedded finance become completely mainstream. Paying bills, sending money, accessing credit, buying insurance—it will all happen seamlessly, often without users realizing they’re interacting with a “fintech product.” These services won’t just live in standalone apps. They’ll be deeply integrated into everyday platforms—merchant apps, messaging services, gig economy tools, even agriculture or education platforms. Finance will become invisible, embedded into the flow of life.

But getting there requires more than just great technology. The public sector has to play an active role too. In many emerging markets, trust in formal financial systems is still fragile. People hesitate to adopt digital finance out of fear—fear of being taxed, of being tracked, or from past experiences with hidden fees or collapsing banks. That trust deficit needs to be addressed head-on. Governments and regulators need to work hand-in-hand with fintechs to build transparency, protection, and digital literacy into the system.

On the product side, I see major evolution in how we underwrite and serve customers. Credit models will get more sophisticated, especially as we gain access to more diverse and behavioral data. Hyper-personalization will no longer be a buzzword—it will be expected. Users will open a financial app and feel like it was designed uniquely for them: their habits, their income patterns, their goals. Financial products will start to feel less transactional and more intuitive, like personalized financial coaching baked into everyday interactions.

Ultimately, fintech in emerging markets will shift from being a disruptor to becoming infrastructure. It won’t be something people “opt into”—it will just be how life works. And if we keep building collaboratively—across startups, regulators, telcos, and traditional finance—I’m confident we’ll get there in the next five years.

Takeaway: Over the next five years, fintechs that invest in customer trust and ecosystem cooperation will likely dominate, especially as open banking becomes more feasible.

Figure 4: Five-Year Outlook for Emerging Market Fintech

Q: What underestimated market trend will likely explode in the coming years?

A: Microloans and micro-insurance are two trends that I think are quietly gaining momentum—and they're poised to explode in the next few years. People are starting to grasp the value of having even a small financial buffer, especially in economies where income is volatile and social safety nets are thin. In emerging markets, a missed paycheck, a medical emergency, or something as mundane as a broken smartphone can quickly spiral into a financial crisis.

That’s where affordable micro-products come in. We’re seeing rising demand for bite-sized financial tools—small loans that bridge a week’s worth of income, or micro-insurance plans that cover a single device, a hospital stay, or even daily work interruptions. These aren’t just nice-to-haves—they’re lifelines. And because they’re small in value but high in frequency, they’re often overlooked by traditional insurers and lenders, which leaves a massive opportunity for fintechs.

What makes this space so promising is that it aligns perfectly with how people actually live and manage risk—on a day-to-day basis, not a year-by-year basis. Whether it’s topping up mobile data, covering a utility bill spike, or replacing a broken motorbike for a gig worker, these are real, recurring needs.

Technology makes all of this possible at scale. With mobile penetration, digital wallets, and better access to behavioral data, fintechs can underwrite and deliver these products almost instantly—and with very low operating costs. That’s something traditional players simply aren’t built for.

So while the headlines often focus on big-ticket fintech stories—neobanks, crypto, IPOs—I think this “quiet revolution” in microfinance will be one of the most impactful trends over the next few years. It’s practical, it’s scalable, and it meets people where they are.

Takeaway: Growing user openness to micro-products suggests a new class of customers ready for entry-level financial protection—and fintechs must meet them where they are.

Disclaimer

ATTENTION - PLEASE READ THROUGH THE FOLLOWING POINTS

The content provided in this newsletter is for informational purposes only and should not be construed as financial, investment, or other professional advice. The opinions and analyses expressed here are those of the author(s) and do not necessarily reflect the views of any affiliated organizations. While we strive for accuracy, we cannot guarantee the completeness or timeliness of the information presented.

Investment Risks

Investing in stocks and other financial instruments involves risk, including the potential loss of principal. It is important to conduct your own research and consider your financial situation and risk tolerance before making any investment decisions. Past performance is not indicative of future results.

No Recommendations

This newsletter does not constitute a recommendation to buy, sell, or hold any security or financial instrument. The author(s) may hold positions in the securities discussed. All information is provided "as is" without any warranty of any kind, express or implied.

Consult Professionals

Before making any financial decisions, you should consult with a licensed financial advisor, tax professional, or other relevant experts. The content of this newsletter should not be used as a substitute for professional advice tailored to your specific situation.

Limitation of Liability

The author(s) and publisher of this newsletter shall not be liable for any errors or omissions, or for any actions taken based on the information provided herein. You agree to hold the author(s) and publisher harmless from any claims or damages arising from your use of this newsletter.

| A guest post by

|

Great! 👏🏻

Wow what a great insight on the Fintech market. 👏